When overtime pay triggers tax confusion

By the time overtime shows up, most households already have a rough system: base pay covers the bills, and the extra hours are the buffer for repairs, debt, or catching up. Then a “no tax on overtime” headline lands and the math stops feeling stable. The paycheck still looks bigger, but it’s not clear whether the whole overtime line would be treated differently or only part of it, and whether the change would hit now or only at tax time. That uncertainty is what makes people over-commit the money or change withholding too fast.

The confusion usually starts with language. “Overtime” on a pay stub is wages, but in tax terms it could be interpreted as the extra premium over the regular rate, not every dollar earned during those hours. If the rule ends up as a deduction, it reduces taxable income only after you add everything up, which means your overtime can still push you into a higher bracket on paper even if a portion later gets carved back out. The timing mismatch is where budgeting mistakes show up.

In practice, the first questions are mechanical, not political: will payroll systems treat the change as a new withholding rule, or will checks look the same and the benefit arrive as a refund next spring? If it’s the latter, the “no tax” benefit won’t help with this month’s groceries, but it could still change next year’s April balance. Until the implementation details are known, the safest estimate is to treat overtime as fully taxable in-the-moment and model any break as a year-end adjustment.

What “no tax” usually becomes in practice

Most “no tax” promises don’t land as a clean exemption on the paycheck line. They usually become a deduction (or exclusion) with limits: a defined maximum amount, a cutoff by filing status or income level, and a requirement that the overtime be separately identified in payroll records. That’s when the benefit starts looking more like a targeted tax break than a blanket rule.

If it’s a deduction, it typically reduces taxable income, not tax owed dollar-for-dollar. So the value depends on your marginal bracket, and it can still leave you owing plenty if withholding didn’t change or if other income (spouse pay, side work) filled up the lower brackets first.

And “no tax” rarely means every tax. Even with an income-tax break, Social Security/Medicare withholding and most state rules would likely keep treating overtime as wages, which keeps the check-to-refund timing gap alive.

Which overtime dollars would even qualify

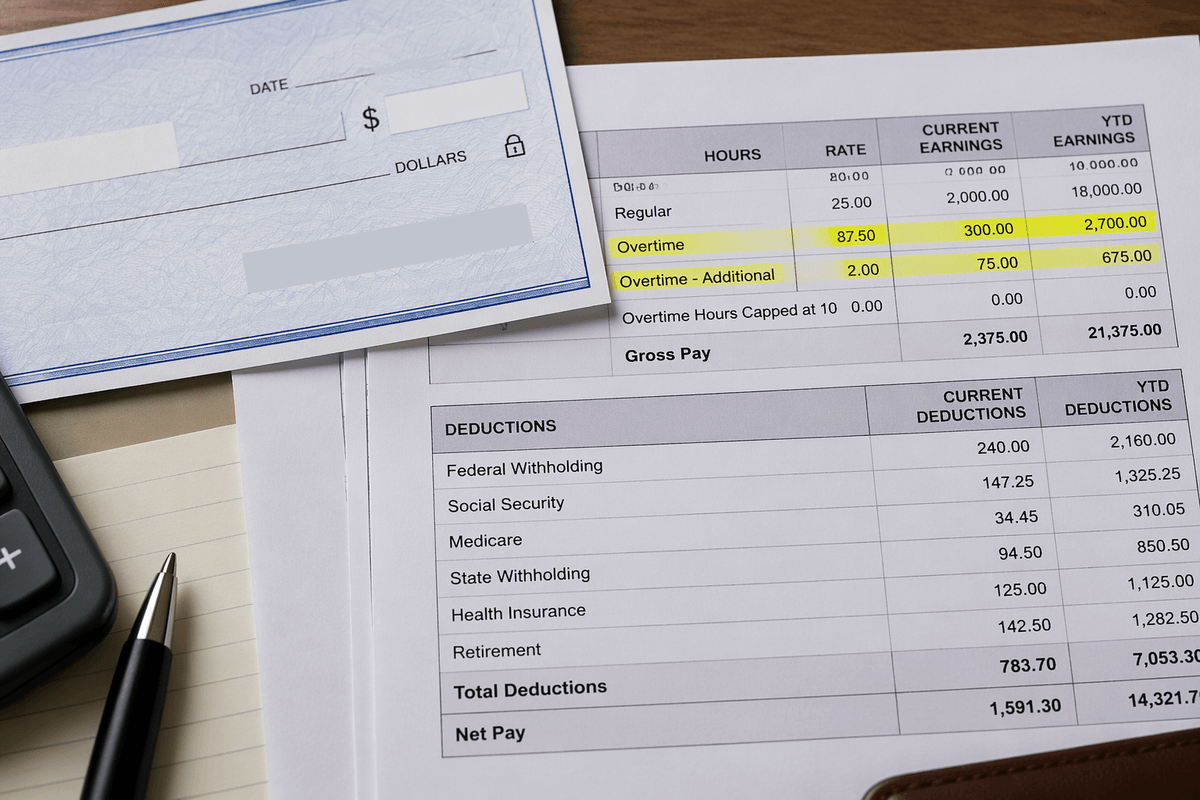

Once you try to estimate the size of the break, the definition problem gets expensive fast. Many payroll systems can identify “overtime earnings,” but that label might include two different pieces: the straight-time pay for those hours and the overtime premium (the extra 0.5× if you’re paid 1.5×). If a deduction is written to cover only the premium portion, the tax benefit could be much smaller than the overtime line on your stub suggests.

It also matters what gets swept into “overtime.” Shift differentials, weekend premiums, and nondiscretionary bonuses can change the “regular rate” under wage rules, which changes the computed overtime premium. If the tax rule keys off a specific payroll code, those adjustments may or may not be captured cleanly.

The practical constraint is recordkeeping: if payroll can’t break out qualifying overtime separately on your W-2 or year-end statement, the deduction may be capped, delayed, or simply harder to defend.

How a deduction changes taxable income math

When the overtime amount finally gets “carved out,” it would likely happen on the return after total wages are already counted. That means your gross income can still look high enough to affect bracket placement, phaseouts, or benefit calculations, even if a later deduction reduces the final taxable income. The friction is timing: the paycheck may stay fully withheld while the deduction only shows up when you file.

In the math, a deduction isn’t a credit. If $3,000 of qualifying overtime becomes deductible, it reduces taxable income by $3,000, and the value depends on your marginal rate. At 12%, that’s about $360 of federal income tax; at 22%, about $660. If you’re already taking the standard deduction, this would need to be an “above-the-line” or separate deduction to matter—otherwise it could get swallowed without changing your take-home.

Withholding surprises on bigger overtime checks

The first place people feel “something changed” is the check itself, and that’s also where the most false signals show up. Payroll withholding tables don’t read headlines; they react to a single pay period as if that pace will continue all year. So a week with heavy overtime can get treated like you just moved into a higher annual income, and federal income tax withholding can jump more than expected. The check is bigger, but the net isn’t bigger by the same proportion, which is where households start second-guessing the benefit.

If the overtime break is implemented as a year-end deduction, withholding may not change at all at first. That creates the opposite surprise: nothing looks “no tax” until you file, and the benefit arrives as a refund or a smaller April bill. People who cut withholding early to “force” the benefit into each paycheck can get pinched later if the rule ends up narrower (premium-only, capped, income-limited) than their estimate.

The constraint to plan around is cash-flow timing. Until employers are told to adjust withholding formulas, assume overtime checks will still withhold like taxable wages, and treat any break as a reconciliation item—not grocery money.

Payroll taxes and state taxes don’t disappear

Even if federal income tax gets reduced later, your overtime check will still run through payroll taxes the same way. Social Security and Medicare are computed on wages, and most proposals don’t touch that. So the “extra” hours keep pulling 7.65% employee FICA (and more if you’re self-employed), and that comes out now, not at filing.

There’s also a ceiling issue. If your year-to-date wages cross the Social Security wage base, that part stops, but Medicare keeps going, and some households hit the additional Medicare threshold later in the year. A heavy overtime stretch can change when those switches flip, which makes net pay jump around even with no policy change.

State and local income taxes are the other constraint. Many states won’t automatically mirror a new federal deduction, at least not right away. The working assumption becomes narrower: maybe less federal income tax next spring, but payroll taxes and most state withholding still behave like nothing changed.

Credits, benefits, and phaseouts get reshuffled

Once a new overtime deduction is in the mix, the “real” cost of extra hours isn’t just your bracket anymore. The deduction might lower taxable income, but your wages still show up high on the return, and that number is what a lot of credits and benefits look at first. If your household sits near a cutoff, a big overtime year can quietly shrink something else—even if you later get part of that overtime deducted.

The most common pinch points are income-based credits and premium subsidies that use versions of adjusted gross income or modified adjusted gross income. If the overtime break is designed as an above-the-line deduction, it could pull those income measures down and restore part of a credit. If it’s structured later in the calculation, you can end up with the deduction helping your tax bill while still losing a benefit that was priced off a higher income figure.

The constraint is timing and predictability: these phaseouts don’t happen smoothly, and one overtime-heavy quarter can change eligibility for the entire year. When you model next year, don’t just estimate tax saved—also stress-test whether that overtime pushes you over a credit or subsidy line before the deduction is applied.

Proof, forms, and what to save now

By the time this becomes real, the benefit will hinge on whether your overtime is separately identifiable, not on how many hours you remember working. If payroll can’t consistently tag the qualifying portion (premium-only vs. all overtime wages), the “no tax” idea turns into a records argument at filing time—right when you’re least able to recreate details from last spring.

Start treating overtime proof like a year-end project. Save pay stubs that show hours, rates, and year-to-date totals, plus any written policy on how your employer codes overtime, differentials, and bonuses. If the W-2 adds a new box or code for “qualifying overtime,” keep a copy of the final pay statement that ties to the W-2 totals so you can spot mismatches before you file.

Also keep the boring stuff: updated W-4 changes, payroll notices, and any mid-year reclassifications. If the rule lands as a deduction with caps or income limits, those documents are what let you estimate the claim without guessing—and avoid fixing it later with an amended return.